Valuing stocks can be complicated at first, there are countless metrics out there and not every metric fits every type of stock. I am not a fan of overcomplication, so let's keep it simple!

Each stock needs to be viewed from its own perspective. If you evaluate all stocks the same way, you will eventually overlook some simply because they do not fit your DCF model or never reach your calculated fair value.

Today we are looking at three types of stocks and how we can value them, we will take a look at value stocks, quality stocks and growth stocks.

VALUE STOCKS (no growth)

Characterizations:

revenue is flat or down

high free cash flow

declining business model

high dividend

high debt

low valuation

Free cash flow yield

For companies with little to no growth the free cash flow yield can serve as a very simple indicator on your return. The free cash flow yield is calculated by dividing the company’s free cash flow by its market capitalization

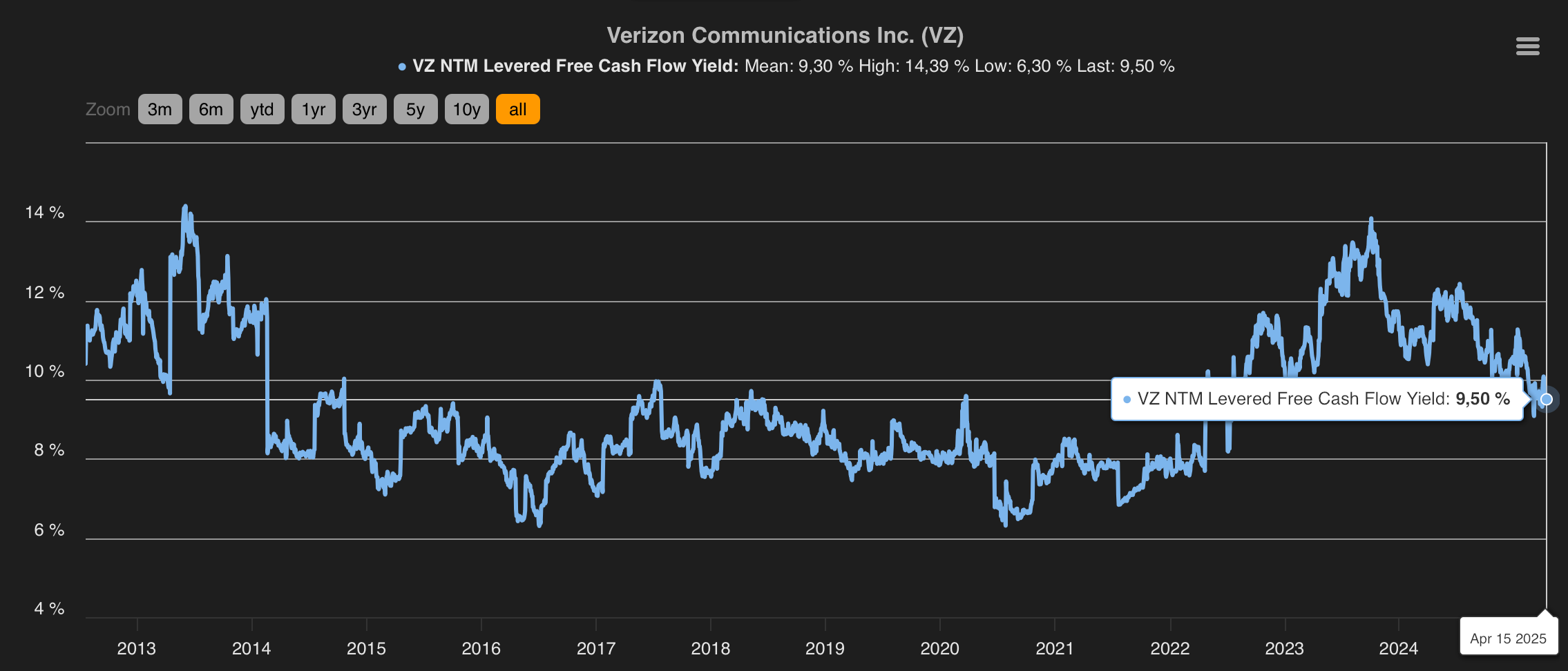

Lets take Verizon as an example. A telecommunications provider based in the US that fits all the characteristics of a value stock.

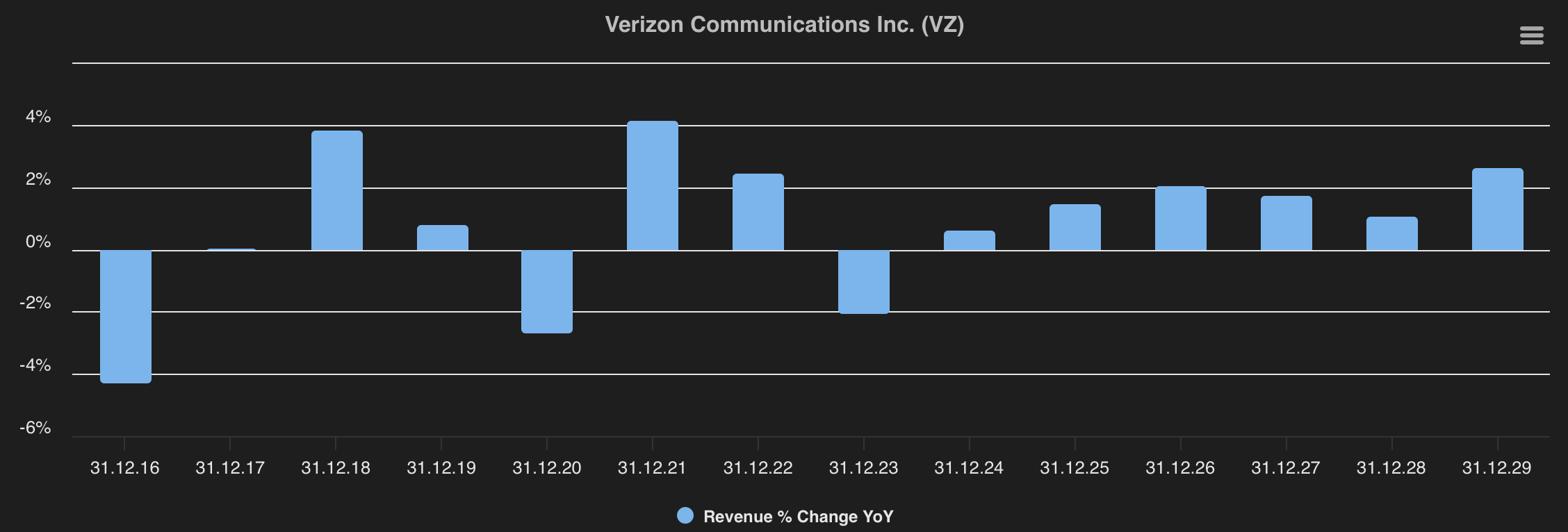

Currently, Verizon’s free cash flow yield stands ar 9,5%. This means that, based solely on free cash flow, you could expect a return of 9.5 percent if you bought the stock at current prices. Below we can also see Verizon’s projected revenue growth is in the range of 1-2%. Adding this to the FCF yield, you could get an 11% annual return with Verizon from here

QUALITY STOCKS (modest growth)

Characterizations:

Consistent earnings and profitability

Strong balance sheet

High return on capital

Stable free cash flow

Modest, predictable growth

Resilient business model

P/E Ratio - EPS Growth

Companies that fit the characteristics of a quality stock should be evaluated differently from value stocks. The reason is simple: Quality stocks will almost never trade at the same low valuation levels.

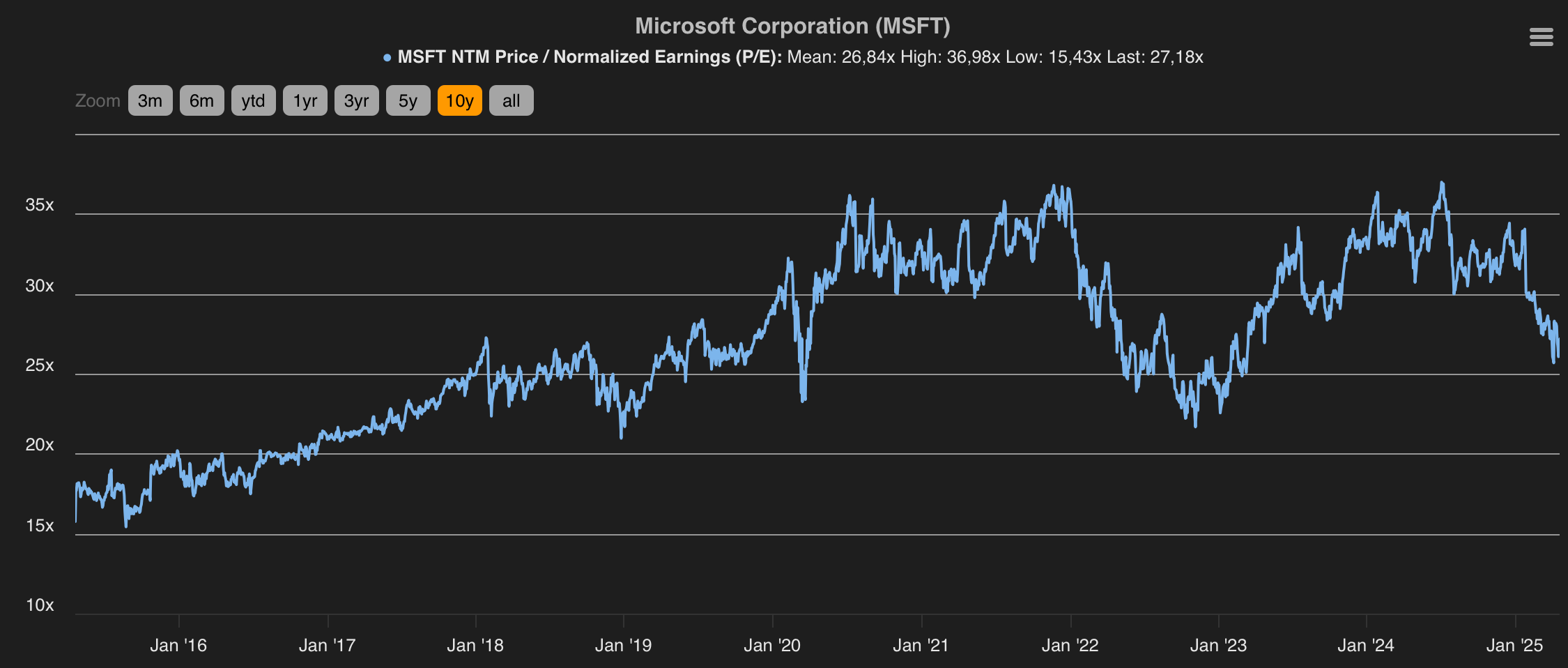

We can use Microsoft as an example. Below we see the forward P/E ratio.Right now, it is trading at around 27 times forward earnings. Its historical average is closer to 24, although it has undergone multiple expansion in recent years. If you want to own Micrsoft and you are waiting for a P/E ratio below 20, good luck. Over the past decade, it has usually paid off to buy Microsoft when it was trading in the low twenties

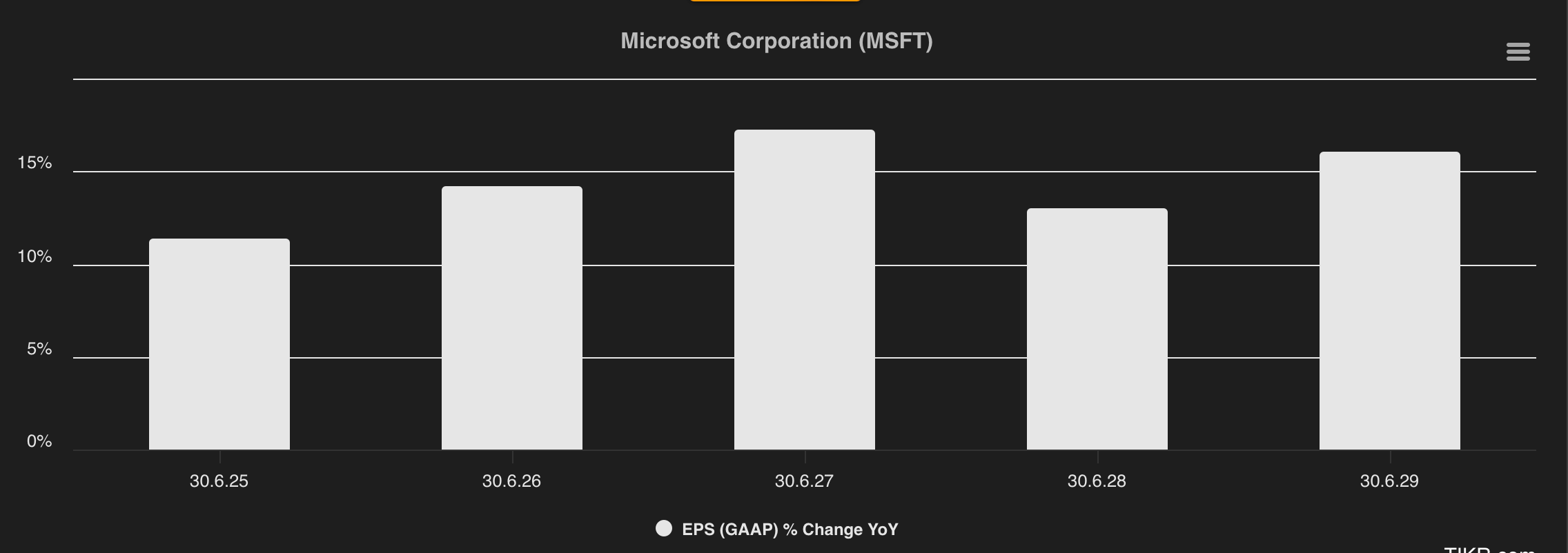

Now let’s assume you buy Micrsoft at 22 to 23 times earnings. The likelihood of it falling much further is low (although anything is possible). At this level, you are probably getting a great deal compared to where it has traded historically. Now if microsoft does not get a multiple expansion your return will come entirely from earnings growth, so between 12 and 17 percent per year. At the low end of that range Microsoft could reach a share price of 508$ by 2029. 623$ at the midpoint and 808$ at the high end.

GROWTH STOCKS (high growth)

Characterizations:

High revenue and earnings growth

High reinvestment rate

Low or no dividends

Expensive valuation multiples

Scalable business model

Future-oriented markets and innovation focus

PEG Ratio

For growth stocks we simply use the the PEG ratio, which divides the P/E ratio by the earnings growth rate. Now, the common belief is that a PEG ratio below one means the stock is underavlued, a ratio of one suggest fair value and anything over one indicates the company is overvalued. With growth stocks, I like to widen that range a bit and look for companies that do not exceed a PEG ratio of 2.

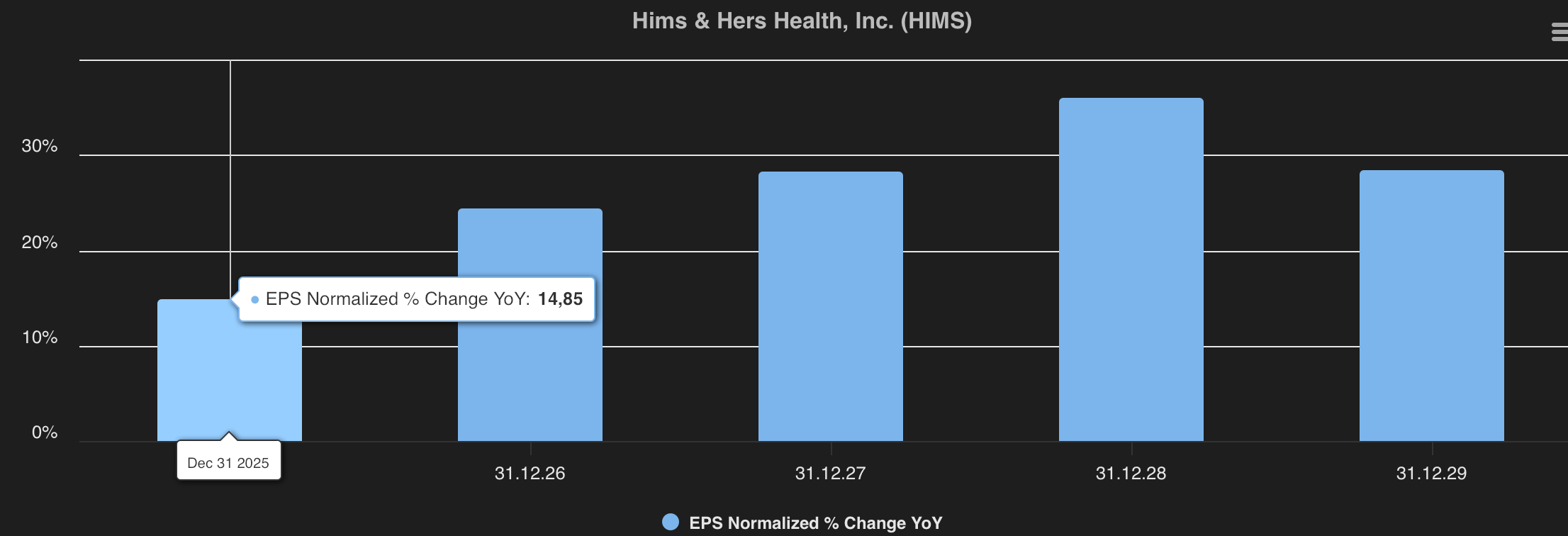

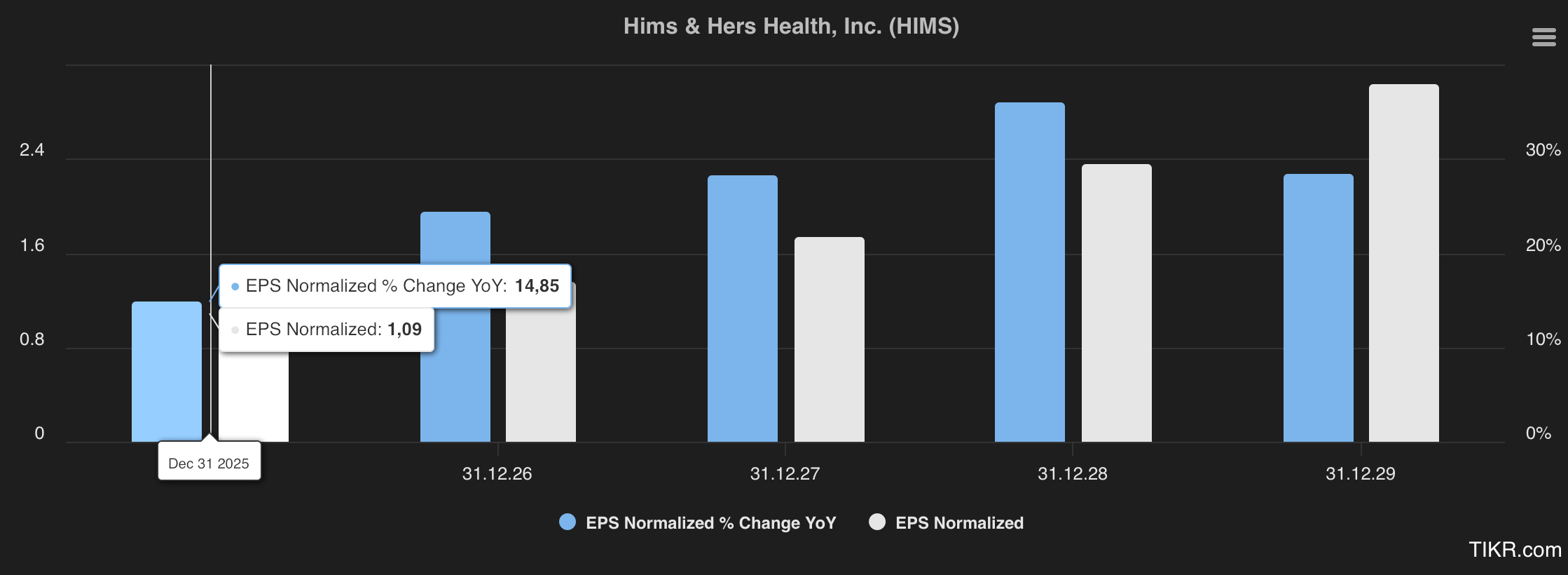

For this approach of valuing stocks we use HIMS as an example. The expected EPS growth for the next year is 15 percent. That means HIMS should not be trading above 30 times earnings if it is to remain within a reasonable valuation range.

This is exactly the case for HIMS! Below we see that HIMS projected EPS for 2025 is 1.09. If we multiply that with double the EPS growth (30), we get a price of 32,7$. This suggests that, based on using the PEG ratio as I define it, HIMS is a buy.

These are just some simple metrics that can help you value stocks quickly and very simple, without spending hours trying to find a fair value. Of course, there are many other factors that need to be considered and that could justify a higher or lower valuation. But if you are looking for a quick way to estimate fair value, these valuation shortcuts can make the process much easier.